A stubborn pandemic held a rally in crude oil prices in check, though Brent crude oil continued its hold on $50 per barrel last week. Headwinds could be developing in commodities given the social restrictions in place in Europe and Asia, while the emergence of a mutated strain of the novel coronavirus that causes COVID-19 is rattling investor confidence. It’s been a tumultuous year to say the least and we’re all hoping for a magic-wand year in 2021.

The price for Brent crude oil moved lower by 1.86% during the holiday-shortened week to end the Thursday session at $51.29 per barrel. We had expected more volatility given the slump that started the week.

The GERM Report held a round table of sorts, getting a perspective on next year from some of our colleagues in the trading and analysis circles.

From the geopolitical side, we expect a President Joe Biden will have a difficult time overcoming the legacy of his predecessor. Trump’s me-first, scorched-earth style of politics has left a sizeable trust deficit for the architect of the power-World War II order. Much ink has been spilled in the volumes of the political journals over the erosion of the liberal world order, the collective body of cooperation orbiting around the ideologies of a United States holding its own vision of Kantian interdependence as a beacon for the world. We expect Biden to hold out olive branches to the likes of NATO, European partners and adversaries like China, Iran and Venezuela. On the former, a Biden administration could ease the strains of the Sino-American trade war through a more cooperative approach. But if the pundits are right, Biden may be forced to try to usher China into an international system that is decidedly different than the Wilsonian world that supported the long peace. What benefit would China get from changing course now?

On the latter, we would expect Biden to ease back on the restraints on Venezuela, once one of the top oil suppliers to the United States. Venezuela’s crumbling infrastructure will create domestic challenges at home and likely limit any malign ambitions from a sanctions-free Nicolas Maduro. Biden, however, will need to be mindful of the Monroe Doctrine and avoid letting Russia solidify its grip on the Americas by courting fringe players such as Maduro, particularly given Moscow’s influence in OPEC. But Venezuela, freed from sanctions or not, can do only so much given the complications at home.

Iran is obviously more complicated. Iranians head to the polls in June to choose their next president and conservative hardliners have made every effort to make this a lopsided race. Incumbent President Hassan Rouhani can’t seek another term and Foreign Minister Mohammad Javad Zarif has declared he won’t run, limiting the influence of some of the more Western friendly voices in Tehran. That leaves it to conservatives, including members of the Islamic Revolutionary Guard Corps who may have scores to settle with the United States after the assassination of Corps Maj. Gen. Qasem Soleimani in January. Iran has and continues to show its resiliency under pressure and with a political clock ticking, Biden will need to move smartly and quickly to bring Iran back to the nuclear negotiating table.

Chinese détente would be net supportive of the global economy simply on the calculus that Trump’s tactics were so destructive. Iran and Venezuela, meanwhile, could balance that growth from Asia with more barrels on the water. Elsewhere, we expect Libya will remain a wild card for commodities and we can’t discount the prospect of conflict given Israel’s U.S.-fed confidence in the Middle East. As lines in the sand become more pronounced, we would expect polar differences to escalate toward the aggressive.

Demand Demand Demand

-Giovanni Staunovo

A lot in the early part of 2021 depends on the collective ability to contain a virus that’s so far been one step ahead of the best that science and social will can muster. A mutated strain of the novel coronavirus has spread beyond the United Kingdom despite the best containment efforts. And we still don’t know for sure what an inoculation based on genetics can do in the long term. Brent will recover, writes Giovanni Staunovo, and oil analyst at UBS in Switzerland, but it will be a difficult journey.

“While we see crude prices trading higher in 2021 and expect Brent to reach $60 per barrel and WTI at $57 per barrel at the end of 2021, investors need to be mindful that the road to higher oil demand and prices will remain bumpy.

We continue to regard higher oil demand as essential for prices to move higher from here, but we believe a material increase in oil demand is unlikely to happen before 2Q21, when we expect vaccines to become widely available. That would help restore global mobility, as it would likely prompt the removal of border closures and quarantine measures.

Currently the Achilles heel on the demand side is the aviation sector. Business-related travel could still be low next year, as companies may make greater use of video conference calls. But we believe this could be largely offset by holiday-related pent-up tourism demand once an effective vaccine is widely available.”

2021 Energy Bifurcation

-Andrew Koval

“Looking ahead to 2021 there are several possible twists and turns for energy markets,” writes Andrew Koval, a macro trader working from Houston. “Aside from the omnipresent COVID-19 economic recovery calculations there are the possible bifurcations from the U.S.-China trade war, the Australia-China trade war and the massive investment we have seen in the electric vehicle and battery markets as special purpose acquisition companies (SPACs) exploded at the end of 2020.”

“Let us focus on the first, China and Australia. Australia is the largest global producer of several of the most ‘necessary’ commodities. China has played big bully and ordered natural Gas and coal imports from Australia. This has spectacularly backfired on China with a brutal winter and not enough of the top-quality coal to keep major cities running, additionally natural gas prices have spiked as they seek alternatives.

“Where does that leave us? There are several possibilities, China is rapidly electrifying its transport, but you need electricity. China is reliant on natural gas and coal. Does this force the Chinese to try to expediate renewables or is the gap too large for now? There are a few possible bifurcations here in the new year.

About electric vehicles, the elephant in the room is rare earth; China is the largest producer with Australia next. Mining rare earth is toxic, as is the disposing of it — the only more toxic waste is nuclear. At some point this will be addressed by a more thoughtful, all-encompassing environmental-aware population. There are alternatives in the works such as hydrogen engines, among others. We have seen a massive surge in capital to this space via SPACs in Europe, the U.S. and UK.

Watch this space unfold and the unintended consequences. What if China’s threats on rare earths lose their importance with alternatives? What if Australia fills missing Chinese exports with Korea, Japan or elsewhere?

What of the large investments by the energy majors in more efficient fossil fuels and renewables? So many variables in this ever-moving matrix of possibilities.

Goodbye 2020 and welcome 2021 and the new possibilities with energy, technology and less timid financial sector.”

The Future of Futures

-Greg Sterijevski

“A year for the record books in more ways than one! It was a year destined to be a wild one given the presidential election in the United States,” writes Greg Sterijevski, a market analyst and founder of CommodityVol.com “However, it eclipsed those expectations. We were disappointed by the conspicuous absence of ET or its cousins!”

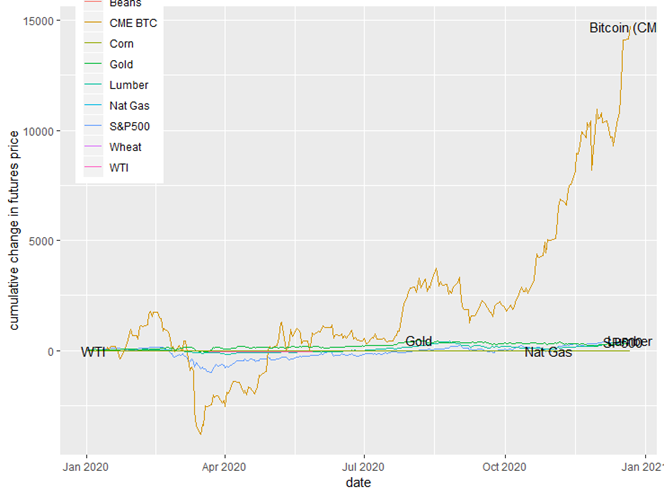

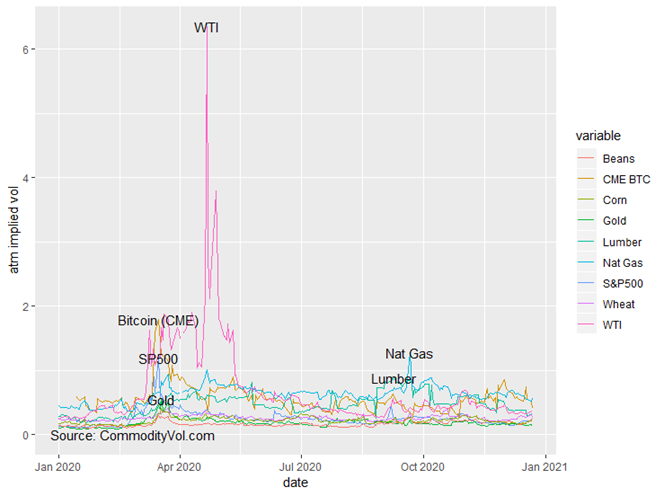

We present only three charts to summarize what happened and offer a glimpse as to what the new year might bring. First is a roundup of the front month futures price.

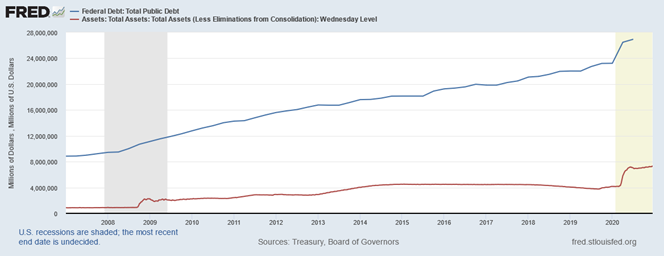

The story of the year was definitely Bitcoin. The futures exploded after stumbling initially on the pandemic in the early part of the year. There are two interpretations one might make of this blistering performance. On the positive, we might say that crypto’s time has come. People are moving toward decentralization and dissolution of control. However, if we add the plot of the public debt and the FED’s balance sheet size we see:

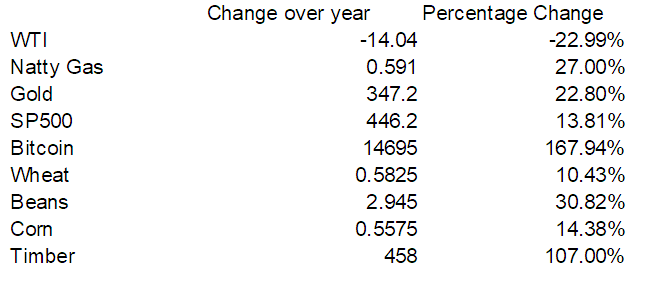

It is hard to not be led to the conclusion that perhaps, just maybe, the run up in crypto is a modern version of speculative excess. Congress has spent money it does not have. It has allowed the government to borrow money that private lenders do not have. The Fed has created hot money to fill in the gap. That money has worked—in cryptos (SPACs, speculative IPOs, …). In tabular form, the following is observed:

With the notable exception of WTI, we see healthy increases in the futures values for all commodities. While the broader equity market as reflected by the S&P 500 was up 14%, the real action was in timber, beans or natural gas. Implied volatility, on the other hand tells a very different story.

The spikes in BTC, SPs and gold all occur concurrently in the March-April period. This corresponds to the rise in uncertainty as COVID-19 concerns became much more pronounced.

The Economy

2021 promises to be an interesting year. It will start with drama around the election, inauguration and transfer of power. The vague promises of goodies to all people made by the new president will run into the realities of the Fed’s balance sheet. Monetization and seigniorage were practices previously consigned to the medieval principalities of Europe and the modern Third World. What capacity will the new government have to plug the gap between $10 trillion in spending and $2 trillion in net taxes (approximate numbers from FRED)? Any move to change the differential tax rate for capital gains will be problematic in the era of Robinhood, and could leave to massive selloffs. The momentum crowd is not as isolated as it was last year. The inclusion of Tesla, for example, assures that any selloff will be felt in the SP. This all assumes that COVID-19 fades into history as a bad memory. In the best case, then, either taxes go up, inflation will go up or a lot of the presumed president’s voter base will be unhappy with the goodies and freebies they get.

The Virus

Let’s engage in some disaster fantasy. If COVID-19 returns, perhaps the immunity conferred by the vaccines is time limited or some mutant strain emerges, then there will be social upheaval of a very base sort. It is said that the Black Death killed off enough people in Europe that it allowed survivors a taste of real freedom. Bands of people could live in depopulated pockets of land without being molested by the local petty tyrant. This taste eventually would lead to the Renaissance. A resurgence of the lockdowns and mandates will lead to this. If death is highly likely from disease, whether I listen to your prescriptions or not, I will not be in any mood to listen to Karen-in fact I might take a swing at a Karen or two. If the vaccines turn out to harm people, or harm people at a greater rate than the virus, the damage to virology and vaccination programs will be multi-generational. No one will trust the people in the white coats. This is the fundamental problem with hyping the virus and the subsequent vaccines. The hype has created an unfavorable convexity. Delivering immunity will not be enough, it must be done without minor side-effects. The upheaval over the MMR vaccine occurred with a very small number of cases over decades. You have an unprecedented mass vaccination of people across wide variations in genetics with vaccines developed in months versus decades. It is my belief that some calamity will occur. The only hope is that the failures will be isolated by easy-to-segment and understand populations.

Abroad

On the international front, the United States under President Trump has formalized several key foreign pivots. Israel is the most important pivot in the Middle East. There is nothing new here, just a statement of what has been tacit U.S. policy since the Reagan administration. In Europe, the pivot towards Greece and away from Turkey seems to be solidifying. Look for the Balkans to be reorganized. That said, the FRED chart looms large here as well. The U.S. operates on the principal of carrot and stick. We show the carrot and then use the stick on the recalcitrant. The carrot is not clear. The U.S. has to borrow (at rates higher than the recipients in some cases) to grow the carrot. The stick is not so stiff either. The U.S. dominance in space and near-space weaponry is under siege by hypersonic weaponry fielded by the Russians, Chinese and possibly the Indians. The Iranian development on hypersonic anti-shipping missiles also seems to be bearing some fruit. These developments will put massive pressure on the armed forces. They must choose to maintain the extremely expensive carrier battle group paradigm or give up and spend the money on the new technology and approaches. Giant bureaucracy rarely gives up. Look for the defense department to keep both-ensuring neither approach gets the resources to give it an honest try.

The Germans are also a key issue in 2021. They have tried subservience, defiance and tribute in order to win Washington over to allow the second leg of the Nord Stream natural gas pipeline to finish. They are most keenly sensitive (in the EU) to inflationary pressures. The outgoing administration has been extremely tough on this point. Biden will be under pressure to mend U.S.-EU relations — and that path will run through Berlin.

The outgoing presidency had one advantage over the previous ones. That advantage was single mindedness (some would say simple mindedness). It is/was about U.S. supremacy with no apologies. A lot of us believe this is hollow. This approach, however, has kept U.S. out of major shooting. The Obama administration’s policy of “humanitarian” interventions and “peaceful” drone strikes will return. The world is a different place. It is the author’s belief that we will suffer a Waterloo moment in one of these foolhardy interventions. Our major competitors (the usual two) do not want any part of an open war with the US. However, supplying a small country with the means to neutralize a carrier or drones is within reason and reach.

Here a Constraint There a Constraint

2021 will be a real test and masterclass in understanding that constraints do exist (see FRED chart above). The fiscal constraints will make campaign promises hard to honor. They will also constrain what can be accomplished in foreign affairs. On the periphery, the U.S. will reorganize the clay that is the Balkans as a tool for its use. It will use the Balkans against the Europeans when it needs to (as the inclusion of North Macedonia in NATO demonstrated). It will act to counter whatever Russian influence exists there. The sums required will be small and there are very few military repercussions. The Persian Gulf is a tender spot as there is a line between the Israel-KSA axis and the Iranians. Since Syria is firmly under Russian control, a humanitarian adventure would probably present itself in Yemen. This is potentially where our Waterloo lives. It would not take too much knowledge transfer to allow the Iranians to control the waters of the Gulf and much of the sky. They can spoil the party.

Negative Convexity Everywhere

The markets associated with retail investors and traders will become acquainted with negative returns. Look for a plunge in financial assets that have so far benefited from blind momentum. Look for subsequent calls for more legislation and a crackdown on swipe trading and possibly crypto. There is massive negative convexity building in all of these assets. The other negative convexity are the vaccines and the virus. Look for the U.S. Centers for Disease Control and Prevention to more stringently count the COVID-19 deaths versus the people who die of something else (of versus with). Look for the CDC to start publishing non-COVID-19 pneumonia and flu death statistics again. The narrative and numbers around the narrative will change to support the story of ‘light at the end of the tunnel.’ The story will change from prevention and vaccination to treatment of those who were infected in spite of vaccination. In the best case, by summer, this will be spoken of as much as H5N1 was during its run. Governments across the world cannot afford more of this and they are aware of it.

2021-Hang on to your socks it is bound to be a wild ride!