Risk level: Yellow

RED: Severe (+/- 4%) ORANGE: High (+/- 3%) YELLOW: Elevated (+/- 2%) BLUE: Guarded (+/- 1%)

THE BOOSTER SHOT

-The US expansion is over.

-We are observing the results of systemic international change.

The largest economic expansion in US history is over, according to the International Monetary Fund. The fund issued a dour assessment of the largest economy in the world as cases of the novel coronavirus continue to accelerate. Standing alone at the top of the international order after the collapse of the Soviet Union, the United States enjoyed a brief moment of unrivaled superiority. The expansion of the shale oil industry later catapulted the United States to a similar ranking among oil producers. But this is not your parents United States and this is not the Cold War order. The global pandemic has triggered claims of systemic change in the international system, where poles of power shift to redefine the status quo. There will be a new normal in the post-pandemic world. Yet the situation is more representative of an effect, not a cause.

Volatility in the price of oil was absent last week. As expected, parties to OPEC+ curtailments agreed to ease back on restraint starting in August even as economists warn of trouble ahead. The price for Brent crude oil went nowhere, relatively speaking, losing only 0.23% on the week to finish at $43.14 per barrel.

US lawmakers passed the Coronavirus Aid, Relief and Economic Security (CARES) Act in March, pumping some $2 trillion into the economy in the form of direct payments to US households, enhanced support for the unemployed and handouts to firms struggling with the quarantine economy. At the end of March, the United States had around 85,000 positive cases of coronavirus and 1,300 deaths attributed to COVID-19. Around 3.3 million people were without work at the time, though the IMF said in its latest assessment that the US economy was under pressure before the pandemic hit. Economists and market watchers spent much of 2019 commenting on inverted yield curves that usually predate a downturn. The latest data show new claims for unemployment dropped for 16 straight weeks, though payroll losses continue to come in at around 1 million in weekly filings, compared with an average of around 200,000 last year. Some 17 million people in the United States were without a job in the middle of June. Nearly 4 million people have the coronavirus and some 140,000 people have died due to complications from the infection. By the end of this month, the financial buffer goes from around $950 biweekly to $350 biweekly unless policymakers decide on additional support. The IMF stated that, even with the high level of federal stimulus, the US economy is expected to show a 37% drop in annualized GDP in the second quarter and a 6.6% decline for all of 2020. The IMF joined a growing chorus of voices in suggesting even more support was needed, including the indoctrination of existing unemployment insurance. That’s unlikely, however, in a political climate controlled by supporters of a president in a state of denial over the health of the economy and of the nation.

“There is a clear need to address trade and investment distortions that are partly rooted in the global trading system’s inability to adapt to long-term changes in the international environment,” IMF economists added. “However, the imposition of import tariffs (and other steps taken by the administration) is undermining the openness and stability of global trade by increasing restrictions on trade in goods and services and catalyzing a cycle of retaliatory trade responses.”

US President Trump rose to power on a wave of nationalist fervor, drawing support from disenfranchised voters who saw the globalized economic system as failing to deliver the goods promised by previous administrations. Trade wars, typically characterized as detrimental to the global economy, are good policy and easy to win, according to this administration. Pre-pandemic economic concerns, however, emanated from the US financial war declared on an ascendant China. This year, a trade war of a different kind – the Saudi-Russian spat over oil market share – decimated large swathes of the energy sector just as demand was eroding under pressure from the coronavirus outbreak. That left some in the US shale patch pleading for artificial market controls reserved only for cartels, the demons of a capital economy.

Much of what you know about the United States is subject to questioning. Asked by veteran journalist Chris Wallace in an interview aired Sunday on the Fox News channel whether the president would honor the long-standing transition of a peaceful transfer of power should he lose in November, President Trump said he’d “have to see.” That is a shocking response for the leader of what could be considered the world’s beacon of democracy and indicative of profound change in the United States. Hope from the tenure of President Obama has been replaced by rage in the era of Trump.

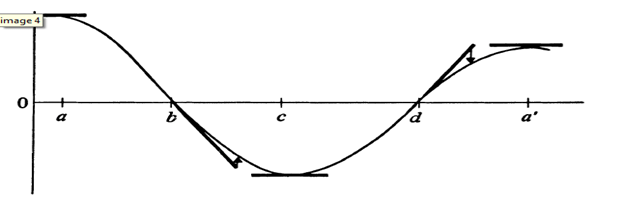

A general system – and the international arena is such a system – has been defined by the ebb and flow of the struggle between a dominant power and an ascendant power. Since Thucydides wrote down his observations of the Peloponnesian War in the 5th century BC, this doctrine has held weight. In the modern era, Charles F. Doran at the John Hopkins School of Advanced and International Studies posited that the power of states follows a regular cycle of ascendance, maturation and decline. What a state wants to do – the way it behaves in the international community – is a function of this cycle. As a nation gains in power relative to others, its capacity to exercise leadership grows; as it falls behind, the capacity – or willingness – to influence international politics wanes.

This behavior tends to follow a pattern similar to economic cycles. “The longest expansion in US history has been derailed by the unanticipated advent of COVID-19,” IMF economists wrote in their latest assessment. Doran and others have charted national power relative to economic power, arguing stability is not seriously threatened during times when trajectory is close to the X axis. But the closer to the apex, the more difficult management becomes.

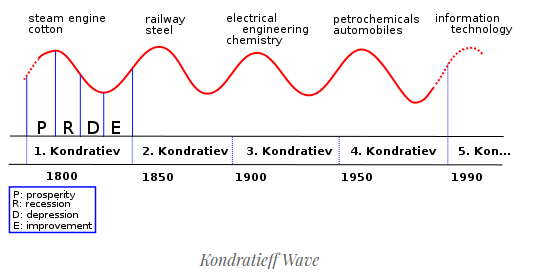

The difficulties of management are put on display in the Trump era, though the current manifestation of US politics is a consequence of disruptive change in the international system that already occurred. Another cyclical examination, while controversial in some circles, is the Kondratieff wave, where changes in the international system occur in regular intervals of some 40-60 years.

Alone at the top of the world with the collapse of the Soviet Union, the United States enjoyed what some commentators have dubbed a brief “unipolar moment.” With no clear adversary, however, the United States fell asleep at the wheel. Extending that wave finds an apex set up nicely during the early aughts, during the advent of the dot com era, and to some degree, the rise of shale. The last apex of the Kondratieff wave also coincides with al-Qaida attacks on Sept. 11, 2001. US President George W. Bush embarked on a war on terror in response, adventuring into Afghanistan and later Iraq to combat the rise of transnational terrorism. Brent Scowcroft, a national security advisor to several US presidents, felt fighting in Iraq made it impossible for the administration to confront more direct national security issues, such as preventing a nuclear Iran. A generation later, Iraq remains in political turmoil and the US conflict in Afghanistan is its longest in history. US shale oil companies are going bankrupt and the economy is in decline. Trump, meanwhile, continues to challenge the foundational aspects of the United States, from open trade principles to containing the aspirations of post-Soviet Russia. The presidency, however, is vulnerable to the currents of international politics. The structure changed on 9/11, though the pandemic has exposed the ugly consequences.

Crude oil prices were under pressure early Monday as European leaders fought to overcome Dutch opposition to a major stimulus package. US lawmakers, meanwhile, have shown little progress in advancing bailouts. European progress could be revealed by Tuesday when European Central Bank Vice President Luis de Guindos takes the podium. Wednesday brings the usual data dump on US petroleum and petroleum product inventories, though pay attention to Canadian inflation and existing home sales in the United States. Consumer confidence in the German economy is revealed on Thursday, though weekly jobless claims in the US economy will almost certainly dominate the headlines of the financial press. The week ends with a flurry of PMI readings for the European and US economies. Front-month trade structures continue to point to an oversupply situation, just as OPEC eases back on constraint. Further contraction for oil prices could be in the cards, though volatility is easing. A Yellow alert is in place for the week, with oil prices expected to move by about +/- 2%.

2 thoughts on “The United States is Long Past Its Pivotal Moment”